| HOME | Project Management Data Warehousing / Mining Software Testing | Technical Writing |

|

This section analyses the freight rate mechanism in the shipping market. Sea transport is a derived demand where shipping demand occurs as a result of seaborne trade. The demand determinants affecting sea transport include government and political factors, the world economy, seaborne commodity trade, average haul, and transport costs. On the other hand, determinants for shipping supply are fleet size and operational efficiency. The shipping supply function shows the quantity of shipping services by sea transport carriers that would be offered at each level of the freight rate, whereas the shipping demand function shows how shippers adjust their demand requirements to changes in freight rates. In the shipping market, the supply and demand curves intersect at the equilibrium price, where both carriers and shippers have reached a mutually acceptable freight rate. Furthermore, the concept of the "shipping cycle" is introduced in this section. A shipping cycle starts with a shortage of ships and increases in freight rates, which in turn stimulates excessive ordering of new ships. The delivery of new ships leads to more supply in shipping capacity. The shipping cycle is a competitive process in which supply and demand interact to determine freight rates. 1. Demand for Sea Transport The shipping business uses the market mechanism to regulate supply and demand. Demand for freight transport is determined by demand for physical commodities in a given location. Because of the uneven distribution of natural resources and specialization of production, some areas experience an oversupply of certain commodities, whereas other areas suffer from a deficit. This geographical imbalance gives rise to the fluctuation in demand for freight transport. In the past few decades, there were occasions when shipping demand grew, stagnated, and then declined. Figure 1 illustrates the determinants of demand for sea transport. The determinants of shipping demand include variables, other than freight rates, that affect the amount of sea transport buyers are willing and able to buy at some point in time. As far as the demand for sea transport is concerned, there are five key determinants influencing shipping demand. The five determinants for sea transport are political factors, the world economy, seaborne commodity trade, average haul, and transport costs.

1.1 Political Factors Political factors cover the strategies adopted by a government. These factors include the government's intervention in trade and shipping matters, as well as the use of trade policies to protect home-made products against foreign goods. Considerations by government bodies on whether to intervene include whether the government is democratically elected by citizens and has predetermined fiscal policies, and whether the country is a member of any economic/ trading bloc and its attitudes towards maintaining membership of international conventions such as the WTO. Other political factors refer to occurrences such as wars, revolutions, national crises, or even strikes. Examples of political events include the Korean War in the 1950s, which led to commodity stockpiling in Western countries; the invasion of Kuwait by Iraq in 1990, which created a tanker boom because speculators used tankers for oil storage; and the incident on 11 September 2001, after which world output grew only by 1.3%, which was only one third of the remarkable growth recorded in the previous year (UNCTAD 2002). 1.2 World Economy An important factor affecting shipping demand is the world economy. After the incident on 11 September 2001, decrease in world output growth led to a reduction in both global export and global import. On the other hand, world output growth has brought an increase in both global export and global import since 2002 (UNCTAD 2005). It seems that the world economy and the demand for sea transport are positively related because the world economy generates demand for sea transport through the export and import of various commodities. Fluctuations in world output growth create a cyclical pattern of demand for sea transport. What is the relationship between the growth of sea trade and world output over time? The concept of "trade elasticity" can be used to describe this relationship. Trade elasticity is the percentage growth in sea trade divided by the percentage growth in world output. In the last three decades, trade elasticity was positive, with an average of 1.4 , indicating that sea trade grew 40% faster than world output growth over this period. 1.3 Seaborne Trade To learn more about the relationship between seaborne trade volume and the world economy, it is desirable to examine seaborne commodity trade. A main reason for short-term volatility (usually within a year) in seaborne commodity trade is seasonality. For example, demand for energy trade can be characterized as a cycle due to a high level of energy consumption in winter in the northern hemisphere. Long-term trends in commodity trade can be identified by observing economic characteristics of the industries that produce and consume the commodities in terms of form (i.e., change in demand for particular products), place (i.e., change in sources from which supplies of commodities are obtained), process (i.e., change due to the relocation of processing plants that change the trade pattern), and time (i.e., change in shippers' requirements to obtain what they desire at designated times). 1.4 Average Haul Demand for sea transport depends not only on the volume but also on the distance over which the cargo is shipped. A ton of iron ore transported from South America to China generates several times as much demand for sea transport as the same tonnage of iron ore shipped from Australia to China. This distance effect is generally referred to as the "average haul" of the trade. Therefore, sea transport demand can be measured in terms of ton-miles, which is defined as the tonnage of cargo shipped multiplied by the average distance over which the cargo is transported. The effect of demand for sea transport on average haul can be illustrated by China's demand for bulk vessel capacity. Recently, China's demand for raw materials has been so enormous that it has exceeded the abilities of its relatively nearby suppliers, such as Australia, to meet its needs for iron ore, coal, and other commodities. Consequently, China needs to expand its supplier networks and source commodities further away from places such as Brazil, Chile, and South Africa. This practice has consumed a large amount of global capacity of bulk ships because more ships are needed for longer voyages. 1.5 Transport Cost In the last century, the development of transport systems, deployment of bigger ships, and adoption of more effective organization of shipping operations have resulted in a steady reduction in transport costs. Reduced transport costs stimulate more demand for sea transport, with an impact on consumers' purchasing decisions, locations of markets, sourcing, and pricing decisions. Consumers make purchasing decisions on the basis of transport costs and product quality. Their product decisions (which affect manufacturers' decisions on what products to produce or suppliers' decisions on where to distribute them) are linked to transport costs and the availability of transport services. Decisions on where to market the products are largely affected by the ability of transport operators to deliver products to markets in a cost-effective manner. Decisions on where to source raw materials or finished goods depend on transport costs. Furthermore, pricing decisions are largely affected by transport costs, which can exert an influence on seaborne trade and long-term trade development. 1.6 Shipping Demand Curve Demand is a functional relationship between the freight rate (i.e., price of sea transport) and the quantity demand for shipping services per time period. The demand curve for sea transport slopes downwards to the right, consistent with the law of demand. The law of demand states that buyers will increase their number of purchases of a product when its price falls, and will decrease their number of purchases when its price rises. A demand curve is a graphical representation of the relationship between the quantity demand for a product (e.g., sea transport tonnage capacity) and its price (e.g., freight rate). When the freight rate changes but other demand determinants remain constant, there is a change in quantity demand. A change in quantity demand refers to a movement along the demand curve leading to an adjustment from point A to point B, as shown in Fig. 2. Shipping demand depends on a number of factors. Seaborne trade is one of the most important determinants affecting the demand for sea transport. An increase or decrease in seaborne trade volume may lead to a change in the demand for sea transport. If any of the determinants for sea transport change, there will be a change in demand and the shipping demand curve will shift. For example, an increase in seaborne trade volume will bring an increase in the demand for sea transport. It shifts the demand curve to the right (i.e., from D to D1) in Fig. 2. On the other hand, a decrease in demand for sea transport shifts the demand curve to the left (i.e., from D to D2).

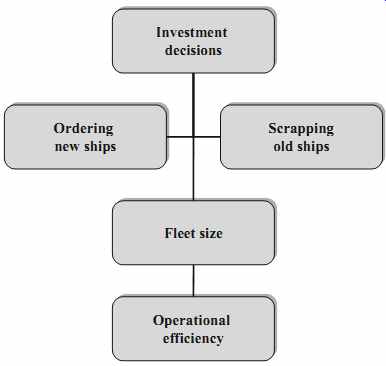

1.7 Elasticity of Demand The concept of elasticity of demand for sea transport is useful for illustrating the relationships between the shipping industry's gross revenue and output and changes in the freight rate. Demand for sea transport is a derived demand. For instance, the demand for tramp shipping depends on the demand for bulk materials. Furthermore, the demand for bulk materials depends on the level of consumption of the final products using the materials. On the basis of these derived demand characteristics, Metaxas (1971) made the following observations: • The elasticity of demand for sea transport depends on the elasticity of consumer demand for the goods shipped by sea. • The lower the cost of sea transport as a proportion of the total cost of the final good, the more inelastic the demand for sea transport will be. • The demand for sea transport will be more elastic if it can be easily substituted by another mode of transport. • The demand for sea transport tends to be price-inelastic in the short run. • The magnitude of demand for sea transport is increasing in the long run as shippers have sufficient time to adjust their shipping arrangements. 2. Supply of Sea Transport Supply of sea transport is measured in terms of the supply of tonnage, which refers to the available capacity for carrying cargo from one or more ports to one or more ports by sea. All the ships that are trading in the freight market constitute "active shipping supply". Ships that are not trading (i.e., laid-up tonnage 1 ), constitute "available shipping supply". All the ships that are suitable for trading (i.e., active shipping supply ) and the available shipping supply constitute the total shipping supply. A unit of measure for estimating the quantity of shipping services produced or available is the capacity-ton-mile per unit of time. To estimate the supply of shipping services, both the cargo-carrying capacity and the distance of the voyage must be taken into account. The shortage of bulk vessel capacity in the past few years has resulted from China's huge demand for bulk commodities, which exceeded the ability of its nearby suppliers, such as Australia, to meet its requirements. Consequently, China feels the need to expand its supplier networks and source from more distant places such as South America and South Africa (Leach 2005). [ 1. Ships not in active service owing to awaiting better markets or needing work for classification. 2. Ships that are trading in the freight market. 3. Ships that are seaworthy but are not trading in the freight market (e.g., laid-up ships). ] The shipping market regulates shipping supply and demand. After discussing the issues of demand for sea transport, this section focuses on the supply of sea transport. The factors determining the supply of sea transport are illustrated in Fig. 3. The supply of ships is affected by four parties: shipowners, shippers or charterers, bankers, and various regulatory authorities. Ship owners decide whether to order new ships or scrap old ships. Shippers influence shipowners by ordering shipping space to transport their cargoes. Bankers influence capital investment as lenders to finance ship purchases. Regulators affect fleet capacity through safety or environmental legislation.

In the long run, deliveries of new ships and scrapping of old ships determine the rate of fleet growth. Owing to the shortage of ships in 2004, investors placed a large number of orders to build new ships. In 2006, carriers added to their global fleets about 110 post-Panamax vessels ranging in capacity from 5,500 to 9,500 TEUs. They also possessed an additional 72 Panamax-size ships ranging in capacity from 4,000 to 5,000 TEUs. As vessel capacity increased by nearly 15%, the freight rate became flat or even declined on certain trade lanes (Clarkson Research Limited 2006). On the other hand, ship scrapping is a business decision dependent on ship owners' predictions of the future operating profitability of ships, as well as their own financial positions. During a recession, if a shipowner believes that there is a low chance of a freight boom in the foreseeable future, it is likely that unprofitable ships will be scrapped. In the shipping market, supply of shipping capacity adjusts when demand for sea transport does not turn out as expected. This market mechanism determines the fleet size in the shipping market. A striking feature of the world fleet in the last few decades is that there have been rapid technological developments over the period. Technical progress and innovations in ship design and operations of vessels have led to jumps in operational efficiency. As a result, bigger, faster, safer vessels can be built, which are capable of providing shipping services at a lower cost per ton-mile, as well as more tonnage for shipping supply. Nowadays, visitors to any large container port are told two things: how big the port's new cranes are, and how deep the port's water is. This basic information is important because new generations of large container ships (which are well over 300 m long, more than 40 m wide, and with a capacity of carrying more than 8,000 TEUs of containers) are being delivered, and they need deeper water and well-equipped terminals. Shipowners prefer big ships owing to the potential gains from cost economies. On a longer time frame, shipping supply can be increased by building more-efficient ships or can be reduced by scrapping old ones. Consequently, the average freight rate can be maintained at lower levels in the long run. The low transport cost makes possible the opening of new trading routes and the expansion of the world freight market. 2.1 Shipping Supply Curve The term "supply" refers to a functional relationship between the freight rate and the quantity supplied by carriers. The supply of sea transport is strongly influenced by the freight rate. The shipping supply function shows the quantity of shipping services supplied by carriers in response to freight rate changes. If the freight rate falls below operating costs, ships will be laid up and supply is consequently reduced. The slope of the shipping supply curve (as shown in Fig. 4) depends on three factors: 1. Bigger ships have lower transport costs per unit of cargo; hence, bigger ships will have a lower lay-up point. This drives smaller or inefficient ships into lay up during recessions. 2. Old ships have higher operating costs so the lay-up point will occur at a higher freight rate. 3. When all the available tonnage is in use, the supply of tonnage can only be increased with higher speeds and improvement in the operations efficiency of ships. Under such circumstances, there will be a steeper slope of the shipping supply curve. Price elasticity of shipping supply measures its responsiveness to changes in the freight rate. During recessions, the supply of sea transport tends to be very elastic when many vessels are laid up. The elasticity of shipping supply is constant at all the levels of output from the lay-up point to a maximum operational speed. The shipping supply is almost totally elastic when vessels' output is severely strained. When all the ships are in service, the supply becomes in-elastic. In Fig. 4, the shipping supply function is a J-shaped curve describing the amount of sea transport the carriers provide at each level of the freight rate. -------------

Ship supply function shows the amount of sea transport offered at each freight rate Freight rate Supply of tonnage Inelastic in supply ------------- 2.2 Short-run and Long-run Shipping Supply How do shipping firms adjust their supply of shipping services? The supply of ship ping facilities cannot expand or contract in the short run. In the long run, there is a time lag between entrepreneurs' decisions to expand their fleets and the actual time of delivery of new vessels. Thus, the supply of shipping services tends to be inelastic and incapable of responding instantly to demand and freight rate changes. "Short run" can be described as a period in which all the fixed factors cannot be adjusted fully. The capital stock, such as ships, and other fixed inputs cannot be adjusted and entry is not free. With respect to shipping supply, Metaxas (1971) made the following suggestions for evaluating short-run shipping supply: • Vessels under construction or under repair for long durations should not be considered as part of the total shipping supply. • Vessels that will shortly proceed to scrapyards for breaking should not be considered as part of the total shipping supply. Considering the points above, it is unlikely that the number of ships will be in creased or reduced in the short run. However, this does not mean that active sup ply remains the same. If the freight rate is above equilibrium and if carriers anticipate an upward trend in the freight market, active supply will increase as a result of the following developments: • postponement of periodic surveys and maintenance; • maximization of the possible service speed at sea; • acceleration of the processes of loading and unloading to reduce the berthing time; • reduction in laid-up tonnage. On the other hand, if the freight rate is below equilibrium and if carriers do not anticipate an improvement in the shipping market, active supply will decrease as a result of the following incidents: • decrease in the average speed of vessels at sea; • carrying quantities of cargo that are less than the maximum cargo-carrying capacity of vessels; • slow operations in loading and discharging; • laying up of vessels. [ 4. A time period sufficiently short where at least one input is fixed (e.g., vessel). 5. A time period sufficiently long so that all inputs are variables.] Depending on the level of the freight rate and carriers' expectations of the shipping market, shipping firms adjust their output in the short run with a view to minimizing their costs and maximizing their profits. In the short run, there may be changes in the magnitude of active supply, but total supply cannot expand or con tract. In other words, the supply of shipping services in the short run tends to be inelastic. "Long run" is a term used to denote a period over which full adjustment to change can take place. It refers to the period in which capital stock, such as ships, can be replaced. It also denotes the time over which shipping firms can enter or leave the shipping industry. The magnitude of supply in the long run depends on the following factors: • the level of demand for shipping services; • carriers' expectations regarding the freight rate of the shipping market; • technical developments as technical progress and innovations in shipbuilding, enabling more efficient provision of sea transport services. Carriers' expectations tend to be high when the freight rate is high. The supply of tonnage can be expanded when entrepreneurs follow one or more of the following courses: • ordering new vessels; • repairing out-of-use vessels. Ordering new ships is a way to increase shipping supply. Breaking up of old ships is a way to reduce shipping supply. Most orders to shipyards are placed during periods of high freight rates, whereas demand for new tonnage is at low levels during periods of low freight rates. In periods of prosperity, demand for new tonnage tends to exceed the capacity of shipyards to supply it. If shipping firms decide to purchase ready-for-use vessels, they may look for ships in the second-hand market. During prosperous periods, the prices of ready-for-use ships tend to be higher than the prices of new ships, which are to be ordered from shipyards. The price of a 5-year-old ship was higher than that of a new building in 2004 (Ocean Shipping Consultants Ltd 2004). This illustrates the importance of time lag between shipowners' decisions to expand their fleets and the delivery times of new ships. As shipping firms seek tonnage supply by participating in the second-hand market for the sale and purchase of used tonnage, prices in the second-hand market tend to follow the market for new vessels. During recession periods, an important factor affecting the contraction process can be the reluctance of shipowners to break up old ships. It is reasonable for shipowners to expect that, as long as the ship remains seaworthy, profitable trading is highly possible in the future freight market. Another factor that can lead to the contraction of ship supply is related to the policy of shipyards. The shipbuilding industry relies on the demand for new ships. Owing to fluctuations in demand for new tonnage, shipyards offer shipping firms attractive terms for new orders, such as low prices or attractive financial terms for ship finance, to stimulate the demand for new ships. [6. A ship is fit in all respects to cope with conditions likely to be encountered at sea. ] 2.3 Rigidity of Supply Shipping is a capital-intensive industry. The costs of increasing or reducing the existing fleet size are high, and it takes about 25 years for the investment in new ships to be recovered. Moreover, since a long time interval (ranging from 1 to 4 years, depending on the capacity of shipyards) may elapse between ordering and delivering new ships, there are significant risks involved in ship investment. Therefore, managers usually do not order extra capacity until a definite trend for increased demand is assured. This situation can be viewed as supply rigidity. There are two types of supply rigidity, namely, institutional rigidity and techno logical rigidity. Technology constraints restrict instant ship supply owing to the time required to build new capacity. In liner shipping, technological constraints are a function of the adequacy of ports and related facilities to accommodate new ships. An example is the intensity of China's export growth since the 1990s, which created congestion at the port of Los Angeles-Long Beach, and the rapidly approaching full-capacity status of the Panama Canal. Modern ships are large and expensive to purchase. Purchasing a ship also in curs a significant financial risk as years pass between ordering and deploying a new ship. Moreover, addition to capacity in ocean shipping is subject to infra structure constraints such as the capacity of seaports, the depth of harbors, and the width of canals. On the other hand, withdrawal of capacity during periods of low demand is costly. Sometimes, it may be more economical to leave ships laid up. This means that capacity is fixed in the short run. How fixed is liner shipping capacity? Fusillo (2004) proposed a stock-adjustment model to illustrate supply in liner shipping. ------------

Sea transport supply function shows the quantity of sea transport carriers would offer at each level of the freight rate Freight rate Sea transport demand function shows the quantity of sea transport skippers would purchase at each level of the freight rate Sea transport demand and supply Equilibrium freight rates ----------- 2.3. The Freight Rate Mechanism The supply of sea transport is influenced by the freight rate. This is a mechanism that the market uses to motivate decision makers to adjust capacity in the short term and to find ways to reduce costs in the long run. On the demand side, the demand function shows how shippers adjust to changes in the freight rate. Figure 5 illustrates the freight rate mechanism. Sellers and buyers transact in the market and their supply and demand requirements cause the price to move. The "going price" is an equilibrium value of the price. This can be explained if we combine the demand and supply curve diagrams. The sea transport demand function shows the quantity of sea transport shippers would purchase at each level of the freight rate. The sea transport supply function shows the quantity of sea transport carriers would offer at each level of the freight rate. The supply and demand curves intersect at the equilibrium price in the ship ping market, which determines the freight rate at which the quantity demanded by shippers for shipping services is equal to the quantity supplied by carriers. At this point, both shippers and carriers reach a mutually acceptable freight rate level. 2.4. Shipping Cycle Shipping cycles play an important role in the shipping industry for managing the risk of shipping investment. A ship is an expensive item of capital equipment. The return on investment of ships depends on the volume of trade. If ships are not invested in but trade grows, then business will come to a halt owing to a shortage of ships. If ships are invested in but trade does not grow, the expensive ships will be laid up. This is the shipping risk pertinent to ship investment. Cargo owners may decide to take this shipping risk when they are confident about their cargo volume in the future. Cargo owners may transport cargoes with their own fleets. This type of operation is known as "industrial shipping". Alternatively, shippers may prefer shipowners to bear such shipping risk, and they go to the freight market to hire ships to transport their cargoes. Under such circumstances, shipowners trade ships and take the shipping risk. For shipping investors, it is necessary to understand the shipping market cycles. 2.4.1 Characteristics of Shipping Cycles Shipping cycles are far more complex than a sequence of cyclical moves in the freight rate. Kirkaldy (1914) considered the shipping cycle as a consequence of the market mechanism. The market cycles create the business environment in which weak shipping companies are forced to leave and strong shipping companies survive and prosper. Fayle (1933) suggested that the shipping cycle starts with a shortage of ships. The increase in the freight rate stimulates overordering of new buildings. Finally, it leads to market collapse and a prolonged slump. The shipping cycle is a mechanism to balance the supply of and demand for ships. If excessive demand exists, the market rewards investors with high freight rates until more ships are built. If there is excessive supply, the market squeezes the revenue with low freight rates until ships are scrapped. 2.4.2 What Causes the Shipping Cycle? The shipping market is driven by a competitive process in which supply and demand interact to determine the freight rate. Excessive demand leads to a shortage of ships, which in turn increases the freight rate. On the other hand, excessive supply of ships leads to a reduction in the freight rate. In general, the shipping cycle is unique, comprising the following characteristics: • The shipping cycle is a mechanism to coordinate supply and demand in the shipping market. • A complete shipping cycle has the following stages: trough, recovery, peak, and collapse. • There are no set rules about the length of each stage. • There is no formula to predict the pattern of the next shipping cycle. 2.4.3 Recent Developments in the Shipping Market Recent developments in the shipping market are useful managerial reference for shipping executives, and are summarized below: • Stage of collapse: Between 1995 and 1998, the container shipping capacity grew at a faster rate than demand. Together with the Asian financial crisis in 1997-1998, this imbalance in supply and demand caused a sharp decline in the freight rate and profitability. • Stage of trough: In 1999, an increase in demand for container shipping services and a low delivery of new buildings led to higher freight rates. In 2000, freight rates remained stable and the balance between container shipping demand and supply improved. In 2001, the growth in international trade was adversely affected by the global economic slowdown, particularly in the USA, leading to another sharp decline in the freight rate and profitability. Consequently, the demand for shipping dropped dramatically. • Stage of recovery: Led by increasing exports as well as imports, China's economy maintained a very positive development, and foreign direct investments in its manufacturing industries persisted remarkably well. Owing to the increasing globalization effect, demand for international container trade showed strong growth during 2002-2003, and freight rates increased significantly across the important trade routes. • Stage of peak: In 2004, world shipping prices were steaming ahead at record levels powered by China's significant increase in demand for import commodities and huge export of manufactured goods to the West. Second-hand vessel prices were high and scrapping rates for old ships were very low. Owing to a shortage of ships, shipowners placed a significant number of new orders in 2004. More new ships were delivered and put into operation in the shipping market; the shipping capacity available in the market became stable in 2005-2006. With a big influx of vessel capacity into the market in the period 2006-2008, there was heavy downward pressure on the ocean freight rate (Traffic World 2005). 2.4.4 Managing the Shipping Cycle Whereas a large ship could have been bought for about USD 32 million in late 2001, a few years later, in 2004, a large second-hand large ship could be sold for USD 62 million (Xinhua Financial Network News 2004). The real money in merchant shipping in the long term is made not only by people who trade in the freight market, but also by people who buy and sell ships at the right time. It is difficult to predict shipping cycles, but it is not impossible to understand the shipping market. Skilled investors use the principle of buying low and selling high. They acquire ships at the bottom of the shipping market when ships are cheap. They sell ships when the peak is reached and take time charters for operations long enough through the trough. Nevertheless, shipping cycles are not "regular". In reality, shipping cycles are loose sequences of ups and downs. Simple rules like the "5-year cycle" or the "7-year cycle" are unreliable tools as decision criteria to predict shipping cycles. There are cyclical booms and busts repeatedly in the shipping market. Careful study of the variables relating to the economic environment, trade growth, new ordering, and scrapping of ships can remove uncertain factors in the prediction. In addition, investors must also consider political issues such as wars, terrorist at tacks, strikes, congestions, and infrastructure developments. The global economic and political environment is complex. Shipping economists need to wait months or years for statistical data to predict the market situation. Under such circumstances, shipowners are more or less in the same position as other speculators when they decide to invest in vessels. Investors in the market must understand the shipping cycle and be prepared to take the shipping risk. Stopford (2004) observed the following characteristics of risk management in the shipping market: • There are both winners and losers in the shipping market. Shipping is not a zero-sum game, but it is pretty close to it. • Shipping cycles are not random. Although highly complex, economic and political forces, which drive shipping cycles, can be analyzed. • Like poker, each player must assess his opponents then work out who will be the loser this time. In the end, no loser means no winner, especially in the sale and purchase market, in which second-hand ships are traded. The job of shipowners is to make the best estimate of the shipping risk that they can afford. These decisions are complex and require decisive actions. For experienced investors, their decisions are based on their experience of past shipping cycles, together with an understanding of the global economic and political environments, and access to up-to-date market information. A good understanding of the market mechanism also helps buying and selling ships at the right time. For instance, vessels aged over 20 years old that were considered for the scrapyard in 2002 were able to earn exceptional money in 2004. The return on one voyage in 2004 could exceed the return from scrapping the vessel 2 years earlier. Also see: Guide to Global Logistics top of page Home Related Articles |